WooCommerce powers 1,079,187 live ecommerce sites as of May 2026. Shopify powers 693,803. That gap is wider than most platform-share commentary admits.

It is also closing fast, but not in the way the headlines suggest. We pulled 18 months of monthly data from HTTP Archive’s Wappalyzer technology detections, covering November 2024 through May 2026.

The standard Shopify vs WooCommerce framing misses the bigger story:

- Hosted platforms are growing.

- Every self-hosted PHP platform is shrinking.

- The rate of decline outside WooCommerce is roughly double what WooCommerce is seeing.

This piece walks through five questions, in order: who powers the most sites today, who gained and who lost ground over 18 months, what the trajectories of the four leading platforms look like, why WooCommerce is slipping, and how badly the rest of the PHP camp is bleeding. We close with what the data means for merchants, agencies, and developers.

Where the Numbers Come From

Every figure in this article comes from the same public dataset. HTTP Archive crawls millions of pages each month and publishes the raw data on Google BigQuery, free to query.

Wappalyzer is the technology-detection engine that fingerprints platforms by HTML signatures, HTTP headers, JavaScript variables, and DOM patterns. The wappalyzer.tech_detections table aggregates the crawl results into monthly counts of active sites per technology, plus the flows of sites adopting and abandoning each one.

We pulled 19 monthly snapshots from November 2024 through May 2026 for 14 ecommerce platforms, all from the mobile crawl (~28M pages per month). The same query can be reproduced by anyone with a free BigQuery account.

Two caveats worth knowing:

- Detection depends on the page exposing identifiable fingerprints. Heavily customised storefronts may be undercounted.

- Deployed-site counts and software-install counts are not the same thing. The WordPress.org plugin page for WooCommerce reports 7 million-plus active installs; our HTTP Archive figure for live storefronts is 1.08 million. The difference is dormant installs, test sites, staging environments, and stores that never went live.

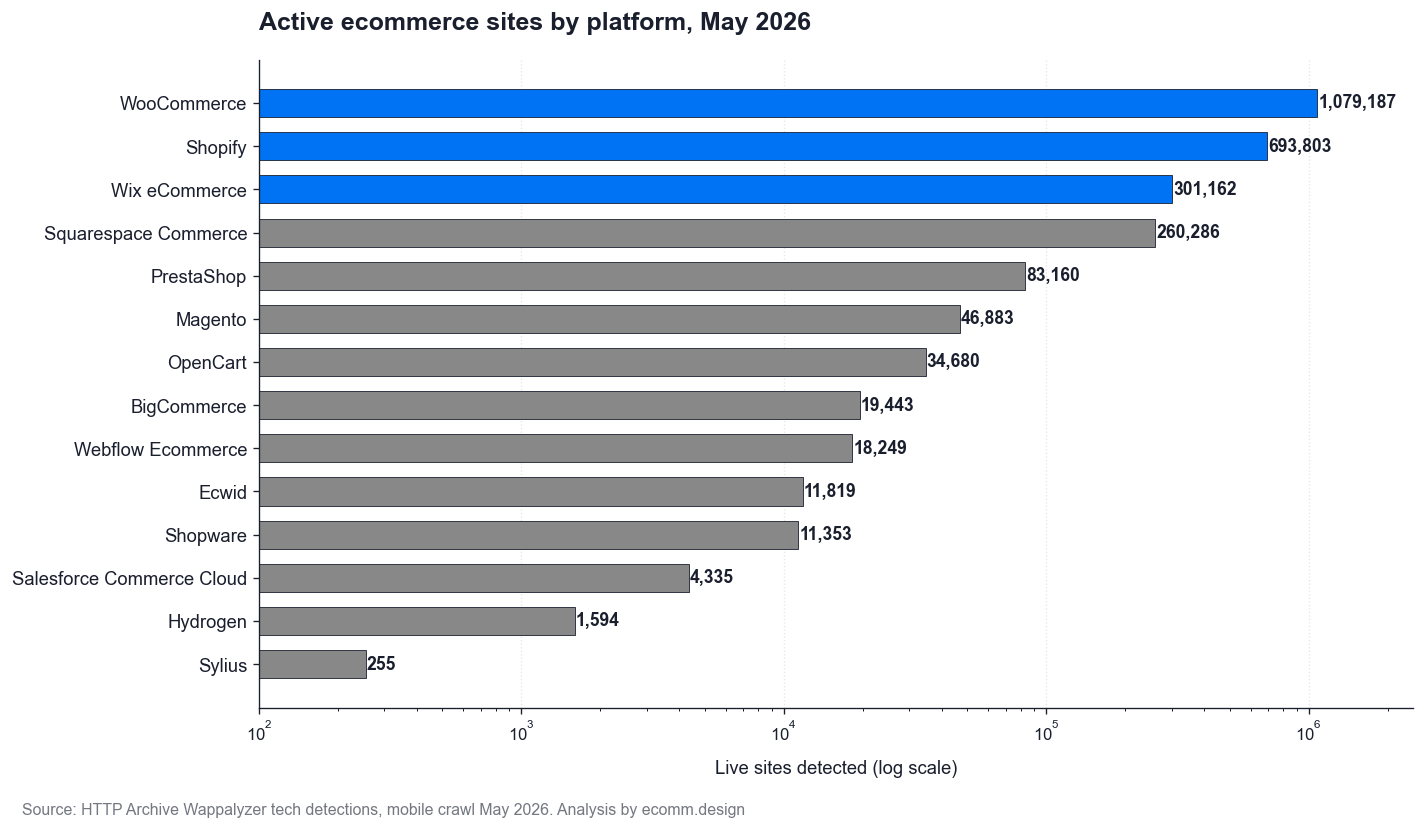

The May 2026 Leaderboard

WooCommerce powers more live ecommerce sites than Shopify, Wix, and Squarespace combined. That single sentence reframes most of what gets written about platform share.

Here is the May 2026 snapshot, ranked by active sites.

| Rank | Platform | Active sites | Tier |

|---|---|---|---|

| 1 | WooCommerce | 1,079,187 | Top four |

| 2 | Shopify | 693,803 | Top four |

| 3 | Wix eCommerce | 301,162 | Top four |

| 4 | Squarespace Commerce | 260,286 | Top four |

| 5 | PrestaShop | 83,160 | Middle |

| 6 | Magento | 46,883 | Middle |

| 7 | OpenCart | 34,680 | Middle |

| 8 | BigCommerce | 19,443 | Middle |

| 9 | Webflow Ecommerce | 18,249 | Middle |

| 10 | Ecwid | 11,819 | Long tail |

| 11 | Shopware | 11,353 | Long tail |

| 12 | Salesforce Commerce Cloud | 4,335 | Long tail |

| 13 | Shopify Hydrogen | 1,594 | Long tail |

| 14 | Sylius | 255 | Long tail |

The top four account for more than 90% of all detected ecommerce sites. Everything below Squarespace is a long tail, and that tail contains every self-hosted PHP option except WooCommerce.

Two numbers worth flagging:

- The gap between Squarespace and PrestaShop is almost 177,000 sites. The four leaders are in a separate league.

- Hydrogen at 1,594 is the most-marketed platform in the bottom half of the table. It is also the lowest-ranked Shopify-owned product on the chart, four years after launch.

BigCommerce at 19,443 deserves a flag too. It is positioned as a Shopify competitor in marketing material but sits an order of magnitude below Shopify on the open web. The middle tier (Ecwid, Shopware, Salesforce Commerce Cloud) collectively powers fewer sites than Wix gained in the past 18 months alone.

A snapshot like this answers “who is biggest right now.” It is the wrong answer to “who is winning.” The order looks very different the moment you measure direction of travel.

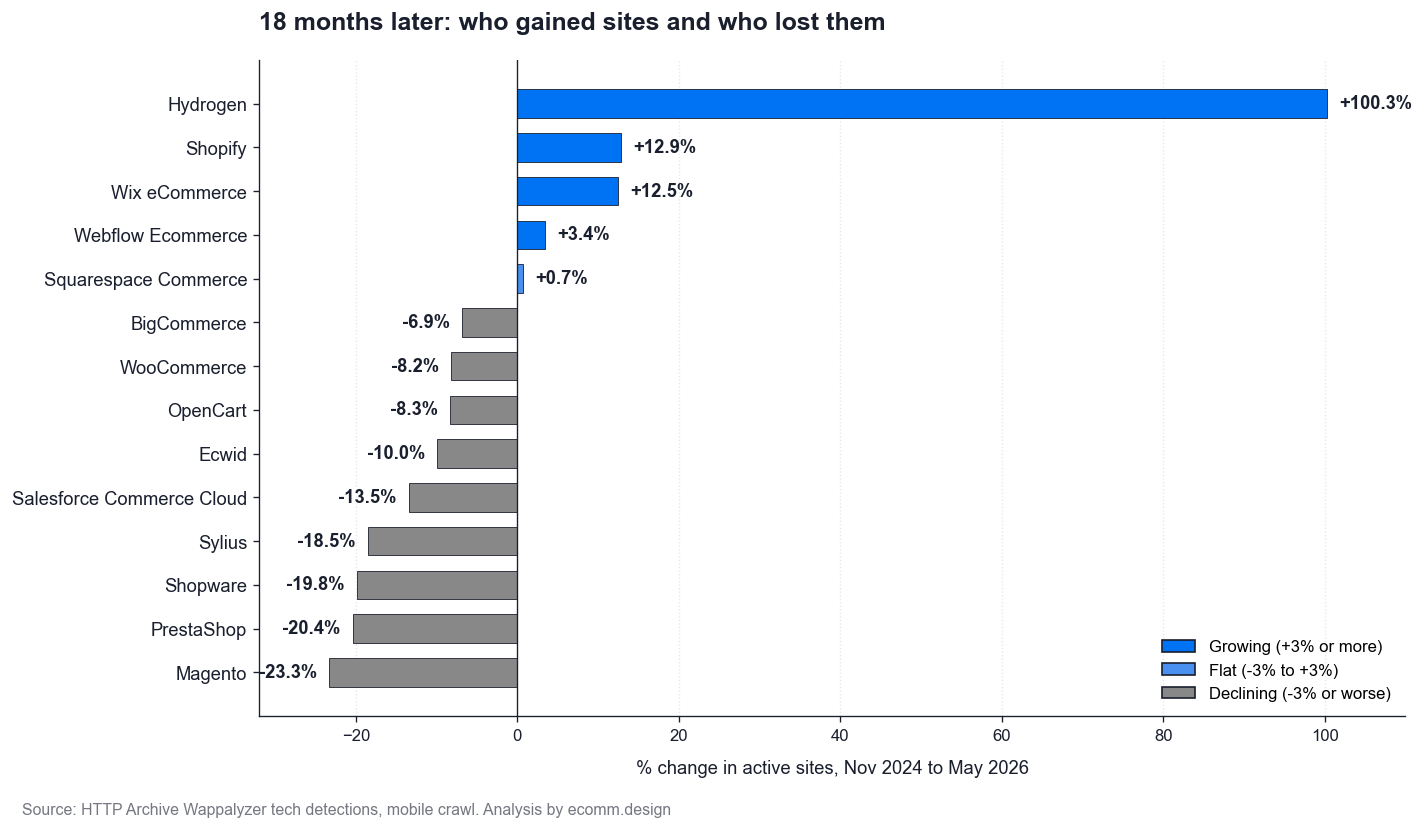

The Direction of Travel

The ranking inverts almost completely when you ask who gained sites and who lost them.

18 months later: who gained sites and who lost them

| Platform | 18-month change | Hosting model |

|---|---|---|

| Shopify Hydrogen | +100.3% | Headless SaaS |

| Shopify | +12.9% | Hosted SaaS |

| Wix eCommerce | +12.5% | Hosted DIY |

| Webflow Ecommerce | +3.4% | Hosted DIY |

| Squarespace Commerce | +0.7% | Hosted DIY |

| BigCommerce | -6.9% | Hosted SaaS (enterprise) |

| WooCommerce | -8.2% | Self-hosted PHP |

| OpenCart | -8.3% | Self-hosted PHP |

| Ecwid | -10.0% | Embedded SaaS |

| Salesforce Commerce Cloud | -13.5% | Hosted SaaS (enterprise) |

| Sylius | -18.5% | Self-hosted PHP |

| Shopware | -19.8% | Self-hosted PHP |

| PrestaShop | -20.4% | Self-hosted PHP |

| Magento | -23.3% | Self-hosted PHP |

Five platforms grew. Nine shrank.

The pattern in the growth column is consistent. Every platform that gained sites is a hosted SaaS or hosted DIY product. Shopify, Wix, Squarespace, Webflow, and Hydrogen all share that property. The customer never touches a server.

Every declining platform is self-hosted, mostly PHP, or older enterprise. WooCommerce, PrestaShop, Magento, OpenCart, and Shopware are all WordPress-or-LAMP self-hosted stacks. Salesforce Commerce Cloud and BigCommerce are SaaS but enterprise-tier and not picking up new merchants at the rate Shopify does.

The migration the data shows is from owned-stack to hosted-stack. Shopify and Wix are the two biggest beneficiaries: Shopify alone added 79,012 net live storefronts; Wix added 33,463. The combined growth of every hosted platform on the list more than absorbs the runoff from the declining camp.

What about Hydrogen?

Hydrogen at +100.3% deserves a footnote. The growth is real, but the base started at 796 active sites and ended at 1,594. Hydrogen launched in November 2021 and is doubling in percentage terms because the absolute numbers remain tiny.

Four years of marketing investment have produced a deployed footprint roughly the size of one mid-tier Shopify Plus customer’s product catalog. The same caveat applies in reverse for Sylius at -18.5%: a slide to 255 sites is statistically real but operationally a footnote against the 14,247 Magento storefronts that disappeared in the same window.

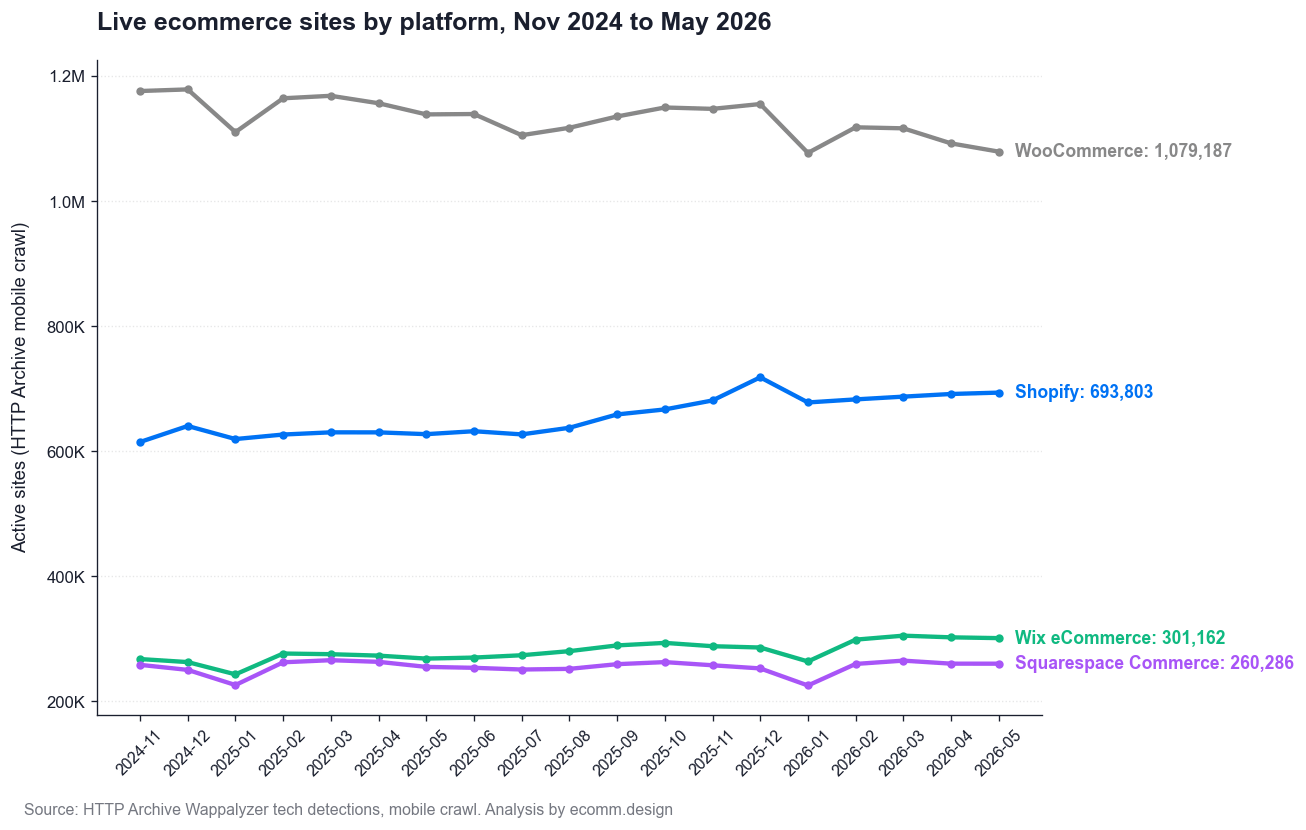

The Four That Matter Most

WooCommerce, Shopify, Wix, and Squarespace together account for over 90% of the deployed ecommerce web. Looking at the monthly trajectories of these four side by side tells the story the snapshot cannot.

Live ecommerce sites by platform, Nov 2024 to May 2026

WooCommerce

Started the period at 1,176,112 sites. Dipped visibly through 2025, bottomed near 1,077,144 in January 2026, and recovered marginally to close at 1,079,187.

Net change: -8.2%, or 96,925 fewer live storefronts. The shape is not a cliff. It is a slow saw-tooth as new sites come online and older ones drop off the crawl, with the churn line edging above the adoption line month after month.

Shopify

Up almost monotonically. 614,791 to 693,803, with very few months of dip. This is the most consistent positive slope in the entire dataset.

The +12.9% gain represents 79,012 net new live storefronts in 18 months. Public Shopify earnings disclosures and our deployment count point the same direction, which is a useful sanity check on the methodology.

Wix eCommerce

Up in near-lockstep with Shopify in percentage terms: +12.5% versus Shopify’s +12.9%. 267,699 to 301,162. Wix crossed 300,000 active commerce sites in early 2026.

Most platform comparisons treat Wix as a tier-2 player. The growth data argues it is firmly tier-1 momentum, just at smaller scale and with a different audience profile.

Squarespace Commerce

Flat. 258,451 to 260,286, a 0.7% change that is within crawl noise. The plateau is the story.

Design-led DIY commerce is mature. Squarespace is holding its position without expanding it, neither gaining from the WooCommerce runoff nor leaking to Shopify.

The bottom line

The old framing was Goliath (WooCommerce) versus growing-David (Shopify). The lines are converging. At the rates of the past 18 months, the WooCommerce-Shopify gap closes by roughly 21 percentage points every 18 months, and there is no obvious reason to expect either slope to flip.

For the merchant choice between the hosted three, see our deeper breakdown of Shopify vs Wix vs Squarespace.

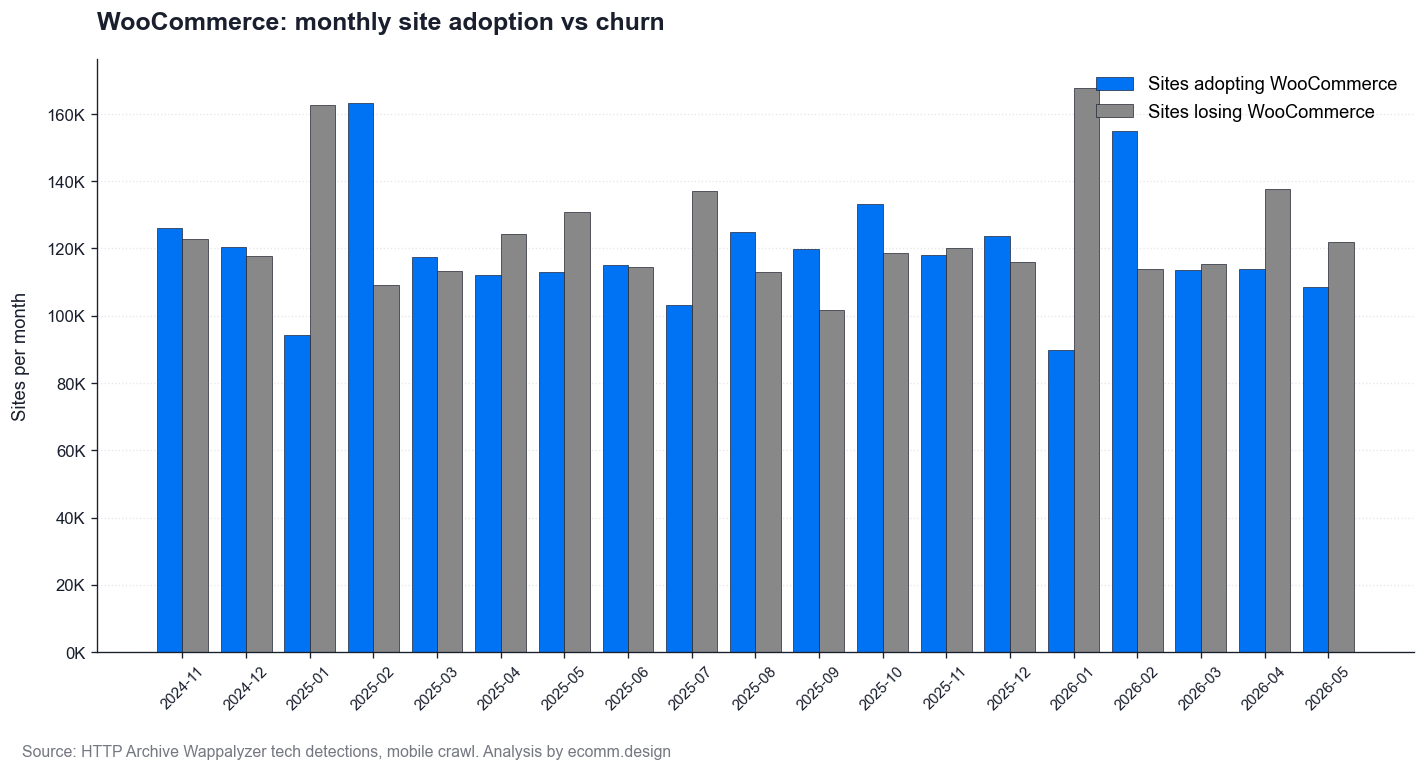

Adoption Is Stable. Churn Is Quietly Rising.

Is WooCommerce declining because fewer sites pick it, or because more sites leave it? Mostly the latter, and that distinction matters for anyone deciding whether to bet on the platform.

WooCommerce monthly adoption vs churn

WooCommerce attracts roughly 118,000 new sites per month on average across the period. That number has stayed flat. The platform is still being chosen at the same rate it was in late 2024.

The other side of the ledger has changed. Monthly churn averages around 122,000 sites and has crept upward, from about 120,000 per month at the start of the period to roughly 134,000 per month by spring 2026.

The decline is a churn story, not an adoption story.

How WooCommerce compares to Shopify on the funnel

| Metric | WooCommerce | Shopify |

|---|---|---|

| Avg monthly adoption | ~118,000 | ~73,000 |

| Avg monthly churn | ~122,000 | ~68,000 |

| Net monthly direction | slightly negative | slightly positive |

| Net 18-month change | -96,925 sites | +79,012 sites |

The two platforms are not fighting for the same merchant from the same starting point. They are running different funnels with different conversion-into-permanence rates. WooCommerce has the wider top of the funnel and the leakier middle.

For an agency, the implication is unambiguous. The WooCommerce-to-X migration market is materially bigger than the X-to-WooCommerce market, and it is growing slowly.

For a merchant currently running WooCommerce, the data does not say anything is wrong with the platform. It says peers are leaving it for reasons that have less to do with the software and more to do with operational fatigue, hosting headaches, and the appeal of someone else’s uptime. Our take on that decision lives in Shopify vs your own website.

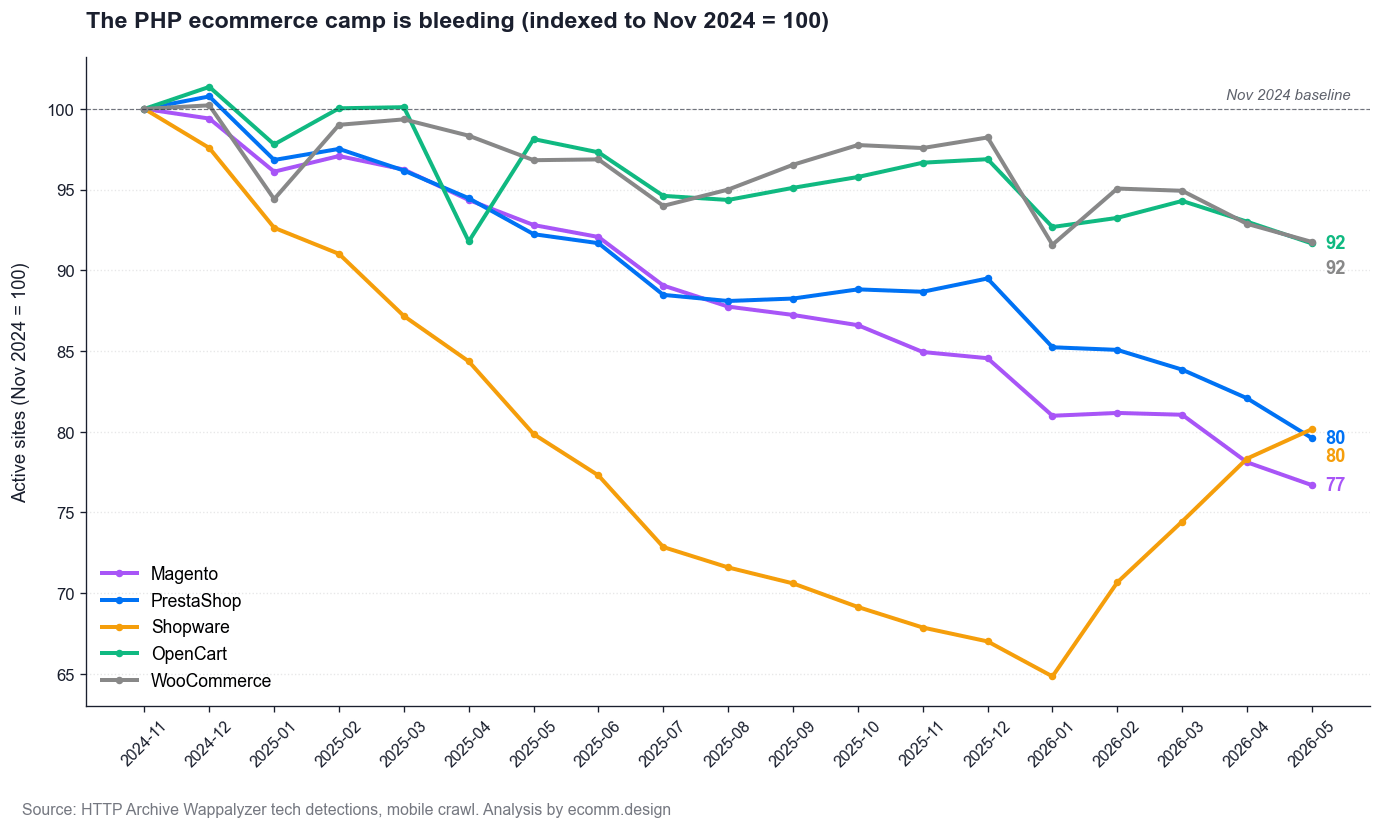

The PHP Ecommerce Camp Is in Faster Decline Than WooCommerce

WooCommerce is the best-performing self-hosted PHP ecommerce platform on the open web. That sounds backwards until you look at the rest of the camp.

The PHP ecommerce camp is bleeding, indexed to Nov 2024 = 100

Indexed to Nov 2024 = 100, every PHP platform we tracked closed the period below 100:

| Platform | Index (Nov 2024 = 100) | Active sites May 2026 |

|---|---|---|

| WooCommerce | 92 | 1,079,187 |

| OpenCart | 92 | 34,680 |

| PrestaShop | 80 | 83,160 |

| Shopware | 80 | 11,353 |

| Magento | 77 | 46,883 |

The ordering is striking: WooCommerce and OpenCart are tied for least-bad, and both are losing sites at roughly half the rate of Magento.

Magento: -23.3%

From 61,130 to 46,883 sites. Adobe acquired Magento in 2018 for $1.68B and has spent the years since pushing the commercial Adobe Commerce edition upmarket.

The community edition Wappalyzer typically detects (Magento Open Source) has not had the investment or the ecosystem updates a healthy platform needs. If you run Magento, our piece on Magento alternatives covers the migration paths in detail.

PrestaShop: -20.4%

From 104,461 to 83,160 sites. PrestaShop is largely a European story.

It never built the global footprint Shopify or WooCommerce has, and the European mid-market is the segment that has moved most aggressively to hosted SaaS.

Shopware: -19.8%

From 14,163 to 11,353 sites. The German enterprise alternative has an active GitHub community (2,088 events on shopware/shopware in April 2026) but is not winning new deployments on the open web at the rate it loses old ones.

OpenCart: -8.3%

Down to 34,680 sites. It is also the platform with the least obvious replacement, which may be why deployments persist.

The takeaway

If your current platform is PHP-based, you are in shrinking company. WooCommerce is the most defensible of the group, but the entire camp is contracting and Shopify is absorbing the largest share of the runoff.

What This Means for Merchants, Agencies, and Developers

The data is not ambiguous, but the right response depends on who is reading it.

For merchants

If you are on WooCommerce and your store works, the data does not say you should migrate.

- WooCommerce is still the largest deployed platform by a wide margin.

- The 7M-plus install base means the plugin ecosystem will outlast any near-term decline.

- An 8.2% drop over 18 months is gentle, not catastrophic.

If you are choosing a platform for a new store in 2026, Shopify has the strongest positive momentum, the largest growing community, and the easiest operations. Wix is right behind on growth and easier still for non-technical merchants, though it is more limited on large catalogs.

The deploy-share trend favours hosted SaaS over self-hosted PHP, which simplifies the long list of options into a short one. If Shopify is on your shortlist, our roundup of the best Shopify themes is a fast way to scope what the front end can look like.

For agencies

The migration revenue is concentrated:

- Magento at -23.3% and WooCommerce at -8.2% with rising churn are the two clearest sources of inbound migration enquiries.

- Shopify and Wix are where most of those merchants are landing.

The strategic move is to build offering muscle around the destination platforms (Shopify especially), the reverse-migration tooling (catalog imports, URL preservation, content migration), and the post-launch optimization work that follows. Our overview of AI Shopify store builders covers how the build-side of those engagements is changing.

For developers

Hydrogen doubled in 18 months and powers 1,594 live sites globally. The growth rate is real and the absolute number is real, but both numbers point to a niche.

- The Hydrogen labour market is small and likely to stay that way for several years.

- The opportunity exists, but it is a bet on the long term, not a generalist move.

The bigger development opportunity in 2026 is Shopify theme work (the platform with the growing deployed base) and headless Shopify integrations that use Hydrogen optionally rather than centrally. Shopify’s theme ecosystem remains the largest commercial opportunity inside the growing camp.

Frequently Asked Questions

Is Shopify bigger than WooCommerce in 2026?

No, not by deployed site count. WooCommerce powers 1,079,187 active sites versus Shopify’s 693,803 as of May 2026. WooCommerce serves 1.55x more live ecommerce sites than Shopify. But Shopify is growing (+12.9% in 18 months) while WooCommerce is shrinking (-8.2%). The lines are converging, not crossed.

Is WooCommerce dying?

No, but it is in slow decline. WooCommerce lost about 97,000 net active sites over 18 months, an 8.2% drop. Adoption has stayed flat at roughly 118,000 sites per month; churn has crept up from 120,000 to about 134,000. The slope points down, but the absolute base is still the largest in ecommerce by a wide margin.

Where do migrating merchants go?

Mostly to Shopify (+79,012 live sites in 18 months) and Wix (+33,463). Webflow gained modestly (+600). Squarespace is flat. The pattern is consistent: leaving a self-hosted PHP platform means leaving for hosted SaaS, not for another self-hosted option.

Is Hydrogen winning?

Not in absolute terms. Hydrogen doubled (+100.3%) in 18 months, but the base went from 796 to 1,594 live sites. That is less than 0.25% of Shopify’s deployed footprint and 0.15% of WooCommerce’s. Real growth, vanishingly small share, four years after launch.

What’s the source data?

HTTP Archive’s wappalyzer.tech_detections table on Google BigQuery, mobile crawl, monthly snapshots from November 2024 to May 2026. The dataset is public and free to query. We aggregated active-site counts, monthly adoption, and monthly churn for 14 ecommerce platforms across the 19-month window.